Two scholars measure the economic impact of VC-funded companies.

Venture capital has become a dominant force in the financing of innovative American companies. | Reuters/Carlo Allegri

Over the past 30 years, venture capital has become a dominant force in the financing of innovative American companies. From Google to Intel to FedEx, companies supported by venture capital have profoundly changed the U.S. economy. Despite the young age of the venture capital industry, a fifth of current public U.S. companies received venture capital financing.

Venture capital (VC) is a high-touch form of financing that is used primarily by young, innovative, and highly risky companies. Venture capitalists provide not only financing but also mentorship, strategic guidance, network access, and other support. These investments are highly speculative — most of the companies that receive VC funding will fail, even as some become runaway successes. Three out of the five largest companies in the world received most of their early external financing from VC.

Clearly, Apple, Google, and Microsoft are among the most innovative and most important companies in a generation. But how important are these and other VC-backed companies to the U.S. economy? How do they compare to industrial behemoths such as General Motors or massive financial institutions such as Bank of America in terms of job creation and overall economic impact? We set out to quantify the long-term impact of VC on the U.S. economy. We started by classifying companies as either VC-backed or non–VC-backed, considering only public companies that are traded on major U.S. stock exchanges. While most successful VC investments end with the company being acquired, reliable information is currently available only on those companies that become publicly listed. Thus, our results likely underestimate the impact of VC on the economy.

We called a company as VC-backed if it was financed in its early stage by a VC fund. Our starting point is the classification used in Thomson One data. We cross-checked that with IPO data constructed by Jay Ritter. We then manually checked more than 200 companies that together represent more than 80% of the market capitalization of the VC-backed companies.

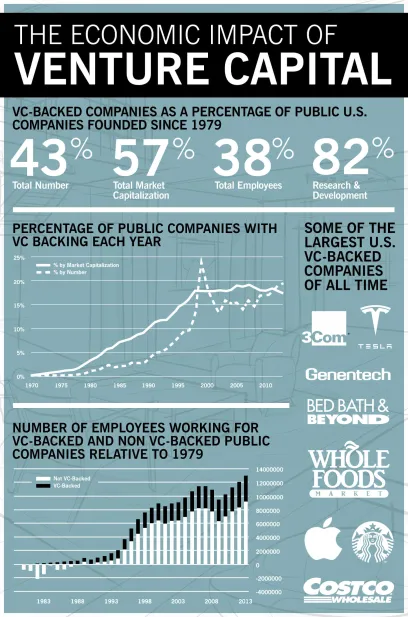

As of December 2013, our sample of public companies had 4,063 firms with total market capitalization of $21.3 trillion. Of those, 710, or 18%, of the companies are VC-backed. Their total market capitalization is $4.3 trillion (20%). These companies tend to be young and fast growing, which explains why their revenue is a relatively smaller fraction of the revenue of the total sample (10%), but their research and development is 42% of the total. That is more than a quarter of the total government, academic, and private U.S. R&D spending of $454 billion. They also employ 4 million people.

This exercise both understates and overstates the importance of VC. We overstate the importance of VC funding to the extent that successful VC-backed companies may well have been successful even without VC financing. Of course, the fact that so many successful entrepreneurs choose VC financing suggests that this financing plays an important role in the entrepreneurial ecosystem.

On the other hand, we understate the importance of VC financing because we ignore the positive spillovers these firms create. From Windows to FedEx, the technologies developed by VC-backed firms have changed the world beyond.

Another major way our previous analysis understated the importance of VC for today’s young companies is because so many public companies were founded before the VC industry even existed. For example, Ford and General Electric were founded more than 100 years ago. While a number of well-known companies were funded by the first generation of the venture capitalists starting in the 1950s, the U.S. VC industry came into its own only after a regulatory change in 1979 that allowed pension funds to invest in VC. That rule change, known as the Prudent Man Rule, led to a greater than tenfold increase in the money entrusted to VC funds: VC funds raised $4.5 billion annually from 1982 to 1987, up from just $0.1 billion 10 years earlier.

To level the playing field, we redid our analysis using only those companies founded during or after 1979. The idea here is to see what portion of the companies that could have received VC financing choose to use VC financing. This exercise excluded the likes of Ford and General Electric, and focused on companies founded since the regulatory changes.

This analysis changed the results dramatically. Of the currently public U.S. companies we have founding dates for, approximately 1,330 were founded between 1979 and 2013. Of those, 574, or 43%, are VC-backed. These companies comprise 57% of the market capitalization and 38% of the employees of all such “new” public companies. Moreover, their R&D expenditure constitutes an overwhelming 82% of the total R&D of new public companies. Given that the VC industry has been in large part spurred by the relaxation of the Prudent Man Rule, these results also provide an illustration of the impact that changes in government regulation can have on the overall economy.

Our results also suggest that the VC industry has leveraged a small amount of capital — when compared to the private equity industry — into investments that resulted in a large number of important companies.

Over the past 50 years, the U.S. VC industry has raised $0.6 trillion and made its investments from that pool. Over that same period, the private equity industry raised four times as much, at $2.4 trillion — four times as much. In 2014, the private equity industry raised $218 billion, almost 10 times the $31 billion raised by the VC industry. In fact, VC funds invest in only 0.19% of new U.S. businesses.

VC-backed companies include some of the most innovative companies in the world. To get an idea of the importance of these companies, it is instructive to look at research and development. In 2013, VC-backed U.S. public companies spent $115 billion on research and development; up from essentially zero in 1979. These VC-backed companies now account for a 42% of the R&D spending by U.S. public companies. That R&D spending produces value for not just those companies, but also the entire world through positive spillovers.

VC-backed companies make up a consistently high fraction of those companies undergoing initial public offerings. Between 1979 and 2013, over 2600 VC-backed companies had their initial public offerings. They made up 28% of the total number of U.S. IPOs during that period. The percentage of initial public offerings that were VC-backed varies by year. That percentage reached a high of 59% during the dot-com boom, but has been greater than 18% in each of the last 20 years.

The VC industry specializes in investing in innovative companies with a huge potential for growth. Because these investments are risky and most of these companies fail, VC funds seek to invest in companies where small investments can generate huge returns. That naturally leads to a focus on certain industries. The industries most impacted by investment have been technology (for example, Apple, Google, or Cisco), retail trade (Amazon, Starbucks, or Costco), and biotechnology (Amgen, Celgene, or Genentech). Industries with higher capital needs, such as finance and primary industries, have seen relatively few VC successes. The small, targeted investments VC funds make are a poor vehicle to finance capital-intensive projects, such as real estate development or mining. While the technologies that VC-backed companies developed have transformed many of those industries as well, our current analysis does not allow us to study that indirect impact.

VC-backed companies play an increasingly important role in the U.S. economy. Over the past 20 years, these companies have been a prime driver of both economic growth and private sector employment. VC-style financing is not the sole reason these companies succeeded; in fact, VC was not even the sole source of financing for many of these companies. However, large and growing fractions of entrepreneurs are choosing VC financing. These entrepreneurs think VC financing is the best way to grow their companies. That makes it clear that VC is an important part of the innovation ecosystem and has helped some of the world’s most successful companies to grow.

For media inquiries, visit the Newsroom.

Explore More

Quick Study: How to Think Like a Venture Capitalist

VCs and COVID-19: We’re Doing Fine, Thanks