There’s a curious pattern that emerges when you start digging into Wall Street trading data from the worst months of the global financial crisis: Several hundred bankers with political connections were bullish on their prospects when it seemed everyone else was not. This group bought shares in their own banks ahead of announcements of new rounds of bailout money and reaped personal benefits, according to a new research paper coauthored by academics from four universities.

The researchers studied trading behavior of bankers during the financial crisis to understand if bankers had predicted the crash or changed their trading behavior during the recovery.

They found bankers with political ties traded their banks’ shares, buying and selling, in the days leading up to a new infusion of government bailout money — reaping benefits to their own stock portfolios.

“Our findings suggest that political connections provided corporate insiders with an advantage during the financial crisis, that a significant portion of this advantage related to knowledge about government intervention, and that some insiders traded to exploit this advantage,” says Stanford Graduate School of Business professor David Larcker, one of the coauthors of the study.

Piqued Interest

The research team — Larcker, Alan Jagolinzer of the University of Colorado, Gaizka Ormazabal of the University of Navarra, and Daniel Taylor of the University of Pennsylvania — were at Stanford as the financial crisis unfolded and were intrigued by trading behavior during an unprecedented period of change in the market.

The first half of 2008 had been challenging for investors. The S&P 500 had steadily lost ground as the year wore on amid concern about the housing market. In March, investment bank Bear Stearns collapsed, and in September, Lehman Brothers, the fourth largest investment bank in the U.S., filed for bankruptcy. By mid-October, the value of the S&P 500 had fallen by 24%.

Concerned that the banking industry might fail, then-Treasury Secretary Henry Paulson rushed the Troubled Assets Relief Program through Congress, which allowed for the investment of hundreds of billions of dollars of federal money to prop up bank liquidity.

In late October 2008, the government made its first TARP infusion, putting $115 billion into the country’s nine largest banks. That first round was mandatory, but successive rounds were optional. Hundreds of banks across the country applied for the program. The Treasury determined who got funding — 705 financial institutions ultimately received $205 billion — but kept the list a closely guarded secret until the official announcement.

At Stanford, Larcker recalled conversations with his fellow researchers as the bailout progressed. The group was curious: Was there any evidence bankers dumped shares in anticipation of the crisis?

Larcker was skeptical. There was so much regulatory scrutiny around banks and bankers during the bailout that he recalled saying he’d be surprised if they found any evidence of informed trading.

A cursory look at the data revealed the opposite: It looked like trading volume among bank executives spiked not before but during the crisis, in the days leading up to new infusions of TARP money.

Larcker and his study’s coauthors were intrigued. Why did some bankers make trades in anticipation of TARP monies, while others did not?

Tricia Seibold

Digging into the Data

Larcker and the team devised a study that examined the trades of 7,301 bank executives working at 497 publicly traded banks from July 2005 to June 2011.

Officers and directors are required to file a form with the U.S. Securities and Exchange Commission every time they buy or sell shares in their banks. The research team used sophisticated computer algorithms to dig through mounds of these disclosures. In total, the 7,301 bank executives in the study bought roughly $1.5 billion in shares and sold $6.1 billion in shares over the six-year period.

Crucially, the study’s authors split the bankers into two groups: Those with political connections, and those without. For the purpose of the study, a banker would be deemed politically connected if at least one person on the board of directors or executive team had worked for — or was currently working at — the U.S. Federal Reserve, the U.S. Treasury, Congress, or a federal bank regulator, like the FDIC.

They divided the bankers’ trades into four time periods: Before the crisis (July 2005 to June 2007), during the crisis but before the bailout (July 2007 to September 2008), during the bailout (October 2008 to June 2009), and following the crisis (July 2009 to June 2011).

For the most part, trading behavior between politically connected executives and their unconnected colleagues was similar in the periods before the crisis, after the crisis, and before the bailout. The researchers found evidence that both groups of bankers failed to predict the crash, with many increasing their stock positions in the months leading up to the financial crisis.

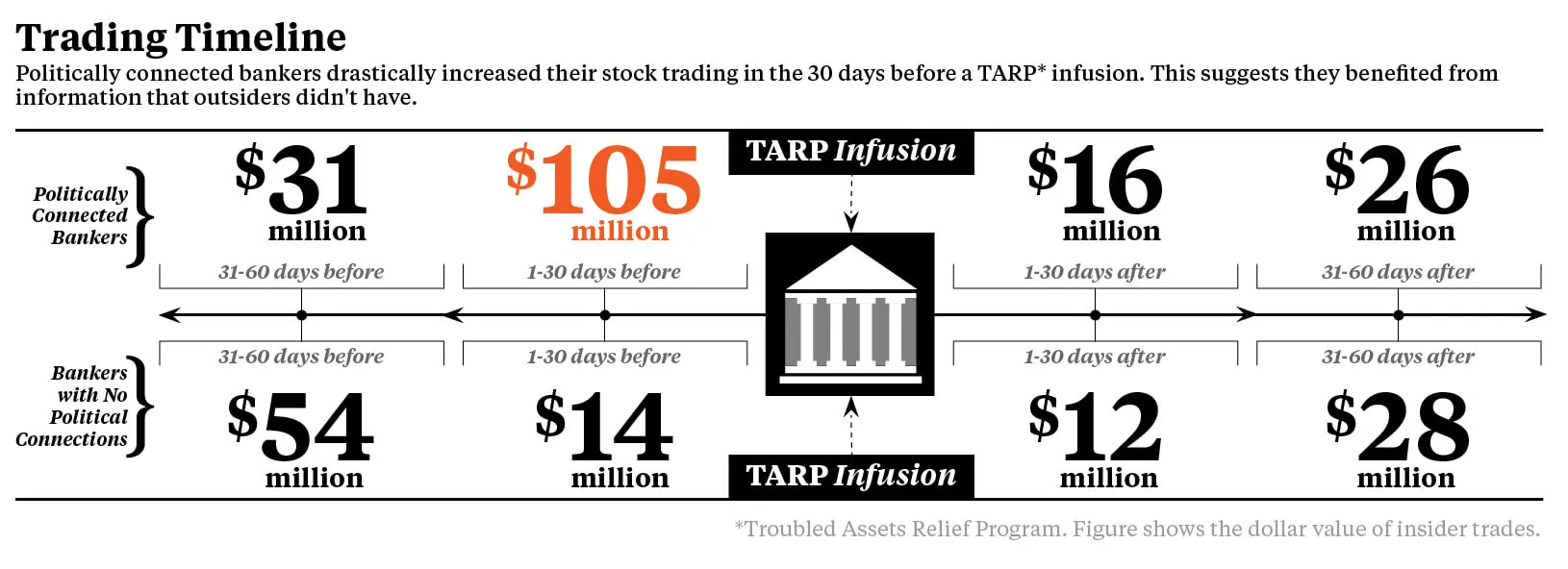

However, the trading behavior of the two groups diverged during the bailout. First, politically connected bankers got more active in the 30-day window before a cash infusion. The researchers found that 30 to 60 days out, this group traded $32 million in shares. But within 30 days, that amount jumped by roughly 250%.

Another major difference between bankers with and without connections related to the size of their stock trades. In the 30 days leading up to a TARP infusion, 150 bankers with political connections traded $105 million in shares, for an average trade of roughly $787,000. Conversely, 233 bankers without political connections traded $13 million in shares for an average trade of about $55,800.

Notably, and perhaps the most striking finding of the paper, was that when politically connected insiders were buying over the 30 days prior to a TARP infusion, the three-day return after the infusion was +4.39%. When politically connected insiders were selling over the 30 days prior to a TARP infusion, the three-day return was -5.13%.

Thus, insiders bought in anticipation of significant prices increases (firms where the market greeted the amount of the infusion as good news) and sold in anticipation of significant price declines (firms where the market was disappointed with the amount of the infusion).

“Collectively, the results from our event study analysis are consistent with politically connected [bankers] trading in anticipation of the infusion,” the researchers write. “They suggest not only that the information content of the trades is related to TARP infusions, but that [bankers] timed their trades in relation to the infusion announcement. This is difficult to reconcile with alternative explanations. At the very least, it suggests [bankers] opportunistically timed their trades relative to the infusion announcement.”

The researchers were careful not to call what they observed insider trading, which is illegal.

“Our analysis casts suspicion on trades of politically connected [bankers] during the crisis, especially those trades that occurred in close proximity to TARP infusion announcements,” they write. “It is likely to be the case that the trades we study fall into a legal gray area.”

For media inquiries, visit the Newsroom.