The world’s largest asset management companies have come out swinging on environmental, social, and governance (ESG) investing, with heavy hitters like BlackRock, Vanguard, and State Street declaring their intention to use their proxy-voting power to press for everything from boardroom diversity to net-zero carbon emissions.

But is that what individual investors really want? Maybe. Maybe not.

That’s the mixed message from a new survey of investors released by Stanford Graduate School of Business, the Rock Center for Corporate Governance, and the Hoover Institution.

The survey, which polled 2,470 investors with savings ranging from less than $10,000 to more than $500,000, revealed sharp differences along generational lines, with younger shareholders saying they are far more eager to have fund managers pursue ESG objectives — and also far more willing to risk higher losses in the process.

Overall, 83% of all respondents said they think their personal views should be considered when mutual fund managers use their shares to vote on environmental or social issues. Their views diverged from there.

While approximately two-thirds of millennial and Gen Z investors said they were very concerned about environmental and social issues like carbon emissions and income inequality, roughly two-thirds of investors 58 years old and older said they were only somewhat or not at all concerned. And while the average investor in their twenties or thirties was willing to lose between 6% and 10% of their investments to see companies improve their environmental practices, the average Baby Boomer was unwilling to lose anything.

David Larcker, a Stanford GSB professor emeritus of accounting and a fellow at the Hoover Institution, coauthored the study with GSB professors Amit Seru and John Kepler, Stephen Haber of the Hoover Institution and the Stanford School of Humanities and Sciences, and GSB researcher Brian Tayan, MBA ’03. Here, Larcker discusses their findings — and what they could mean for fund managers.

Why survey individual investors in big funds about their personal attitudes toward ESG investing?

The whole ESG push has been remarkable: lots of money flowing in and lots of discussions about climate, diversity, and all those important things. But the debate about what we should do going forward is complicated, because there are a lot of hidden assumptions about what people are claiming.

One assumption is that there will be market pressure to respond to stakeholders’ ESG objectives and preferences. That makes sense, but where’s the evidence that it really is true, and that it has a substantive impact on companies’ behavior?

Also, these are societal issues, but it’s not like everybody has a homogeneous point of view on ESG topics. All the big mutual funds are making statements about wanting companies to embrace diversity or net zero or whatever. But what do stockholders really want mutual funds to do in terms of voting or pressuring companies on ESG issues?

As ESG proposals come forward, fund managers have a fiduciary responsibility to vote up or down on them. We’re backing up a step and asking, “Are you voting in a way that’s consistent with the objectives of your shareholders? Do you actually even know anything about that?”

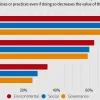

In general, the investors you surveyed were most willing to lose money in pursuit of environmental objectives, and least willing to suffer losses in the name of good governance.

Environmental and social issues are much more understandable and personal to people. Is your water bad? Are there way too many people in your community living below the poverty line? Those are issues people understand very well, and that they experience firsthand — as opposed to, “Is the board made up entirely of independent people?” That’s a little more abstract.

Most also agreed that fund managers should take investors’ views into account when voting on environmental and social issues. But whether they wanted fund managers to wield their voting power to press for progress on those issues — and whether they were willing to lose money as a result — depended on how old they were.

People my age tend to say, “We want you to reflect our opinions, but our opinion is that we don’t want to lose any money in our accounts to satisfy some ESG objective.” Whereas younger people seem to be willing to give up a bit of their investment for things that they view as socially or environmentally good. They’re not willing to give up everything, but they’re willing to give up some.

What we’re trying to get a handle on is, if these investments are not positive for shareholder value, what’s the trade-off? How much are shareholders willing to give up to deal with wealth inequality, for example? That would be a useful input into the decision making of these funds with regard to their voting behavior, or when they meet with management saying, “Hey, here are the things that are really important on our list, and here’s why.”

What accounts for the split between younger and older investors?

Older people have a shorter time horizon; if they lose a bunch of money because their fund moves big-time into ESG, they won’t have much time to make it up. If you’ve got 30 to 40 years to do so, it’s less painful.

But something else is going on too. Older people think that returns are going to be fairly low in the coming years. They also think that they have a pretty poor understanding of how market prices move. Younger people, meanwhile, are much more optimistic about returns, and they feel very confident in their knowledge.

Now, if you think that prices are going to go up every year by 10% or 15%, you might be willing to give up some of your nest egg because it will still grow to become fairly big. If you think that growth will be much lower — which is how older people look at it — then your internal arithmetic is going to be different.

How should fund managers deal with these strong differences of opinion?

Maybe it would be a smart move to poll your investors to see what they want, particularly on issues where there’s a pretty good chance that if you really tilt your investment strategy toward ESG, you’re going to incur a loss. They’re your customers and you have fiduciary responsibilities to them, so take their preferences into account. Let’s say an ESG proposal is being voted on at the annual meeting; you poll your people, and 60% like it and 40% don’t. Maybe you should split your vote.

For media inquiries, visit the Newsroom.